Note: we interviewed an expert for this article but due to PR concerns from one of his employers we were unable to give him the credit he deserves. If you have questions, reach out and we can connect you as necessary.

You know the number one complaint about payments acceptance?

It’s too expensive.

Merchants everywhere rightly believe that the cost to move money should be zero. If people need credit, perfect, let them pay interest on credit extension and fund the movement of money. But shelling out 3%+ just to accept payments?

Usury.

One of the hidden costs of payments acceptance is hardware.

Hardware that’s clunky, expensive, and programmed in a way that requires the merchant buy all new hardware to move payment providers.

We’ve exposed some of this previously, but imagine shelling out $600 for a device that sits on your countertop and does nothing else but accepts cards.

$600.

You can buy a good, modern desktop computer for $600.

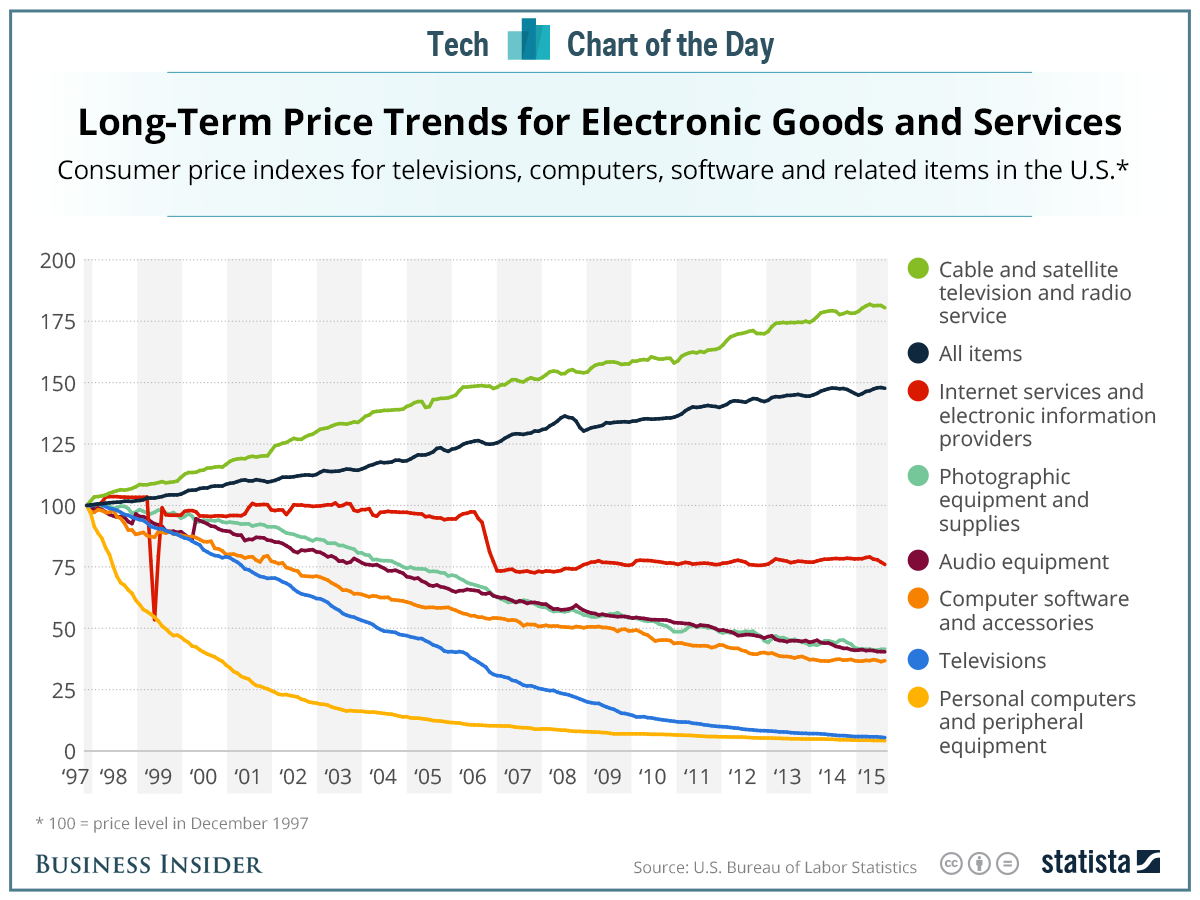

Look at this chart of electronic goods and services costs over time. Note that the only two lines that aren’t rapidly decreasing are the monopolistic utilities of cable and internet (these are akin to Visa and Mastercard with infinite pricing power).

Everything else has decreased logarithmically in cost.

Meanwhile, somehow, you can buy 6 new Android tablets for the price of a single-purpose payment terminal.

Don’t believe us? Look at the length of the list of Android devices under $100 on Amazon.

245 pages of 40 devices per page = 10,000 tablets that are superior to a terminal:

- Have better processors, OS, battery, memory, connectivity, and displays than terminals

- Can be used for tons of things besides taking a payment

- Are better in every way, the end.

Think of an average merchant doing $500K in annual processing volume. They buy two terminals for $1,200. That’s 0.24% of revenue. If you imagine they negotiated payments at 20 bps of margin, the cost of this hardware is MORE than they’re paying in payments margin.

Then they learn that they’re being boned by their payment provider and want to move to a new provider. Odds are that these terminals can’t be reprogrammed and the merchant is back on the hook for another $1,200 to move to a more honest payments partner.

Enter SoftPOS.

SoftPOS was pioneered by fintech startups like MyPinPad and Mobeewave, which Apple later acquired to serve as their core technology for Tap to Pay on Apple devices.

In 2012, when the idea of accepting payments on a mobile device was first conceptualized, these companies focused on using the technology to free merchants from existing payments hardware, which was unreasonably expensive and limited to a physical environment. It took half a decade for the industry to put a standard in place, but in 2017 the PCI Security Council released SPOC (Software PIN on COTS).

For the first time SoftPOS providers had a technical standard they could bring to market.

Despite the obvious benefits and a new specification, SoftPOS providers were still seen as a niche solution. This changed in 2018 when an influential but unnamable person connected with Montreal-based Mobeewave. Having spent almost a decade in the telco industry, this resource was fresh in payments and instantly recognized the potential impact for SoftPOS.

Working with Visa and Mastercard, this person helped launch Samsung POS in October 2019 using Elavon’s payment rails and Mobeewave’s technology on Android. In a world first, merchants could submit a merchant application on their Samsung device and, if approved, accept payments in under 15 minutes.

SoftPOS was firstly created to meet consumers where they are. With the proliferation of mobile devices, countertop terminals would fall far short of necessary payment flows. Mobile commerce is eating desktop commerce and the mobile phone has become one of the most important devices a person carries. Think about it: when you leave your house what are the three things you have on you at all times? Your wallet, your keys, and your phone, and the phone is even replacing those first two.

What exactly is SoftPOS?

At a high level most SoftPOS platforms are like an EMV Certified Gateway. The SoftPOS application allows a COTS (Commercial off the Shelf) device to accept payments via the NFC Chip. This includes both payment cards and wallets via other smartphones or tablets.

The problem is that people keep looking at SoftPOS as a terminal. SoftPOS is a software layer that can enable payments on any platform, irrespective of device. It can fit anywhere. Every single mobile app out there IS what SoftPOS was designed to support.

The US payments industry has normalized merchants to the point where they accept an expensive piece of hardware that sits on their countertop to accept payments. It probably wasn’t any different 20 years ago when merchants were forced to accept knuckle-busters and the interminable number of carbon copies lying around.

SoftPOS can be installed on any NFC-compatible device to accept payments. This means a merchant can turn a $100 tablet into a credit card terminal so long as the customer is willing to pay in a contactless manner, either using the contactless feature that’s native in most credit and debit cards, or a digital wallet on their phone which itself is NFC-enabled.

And paying with SoftPOS on a consumer’s phone comes with manifold security benefits that reduce fraud to essentially zero.

SoftPOS platforms are future proofing for BLE (bluetooth low energy) and biometrics (part of existing EMV specification) to confirm that the person transacting is where they say they are and who they say they are. While this isn’t ubiquitous today, the infrastructure is there to allow SoftPOS to be one of the most secure if not the most secure method of payment available.

In a real vote of confidence, the world’s most profitable retailer by revenue per square foot has gone all-in on SoftPOS. So much so that they actually acquired the technology.

Apple previously allowed their employees to take payments in their retail stores on their iPhones with a custom Ingenico sleeve, but now Apple has gone directly to mobile devices using SoftPOS. Apple uses SoftPOS because it makes retailing that much more convenient for all parties, ultimately fulfilling Mobeewave’s vision for SoftPOS: meeting commerce where it happens.

Apple shouldn’t be the only retailer that adopts SoftPOS if for nothing else than its device management benefits.

Look at the below image from a restaurant. Then look at all the devices in that environment.

In a traditional Retail or Restaurant environment, managing these devices from an IT perspective is a real pain in the ass. At a minimum it’s costly, especially with traditional payment terminals. Thankfully most of the terminal manufacturers are adding Mobile Device Management (MDM) capabilities which allow remote administration and tracking of the device. For any merchant with multiple locations this is critical.

Smartphones and tablets have such a massive advantage in that they natively work with a wide variety of MDM tools and services, making SoftPOS extremely viable for enterprise level merchants with large IT teams that have always struggled to manage payments within technology stack. SoftPOS – and therefore payment acceptance – simply becomes a feature or an app they can push to any compatible device on their network. With managed services becoming viable for smaller merchants, it makes sense to see SoftPOS become more widely adopted.

Given its myriad benefits, why don’t we see more SoftPOS today? If we eliminate ignorance and self-interest in hocking $600 countertop paperweights as possible explanations, the following are legitimate reasons why SoftPOS hasn’t yet taken over the world.

The first impediment would seem to be devices for SoftPOS payment acceptance, but a bit of research shows that’s not a real concern. Back in 2012 when Mobeewave launched, few mobile devices were NFC-enabled. As of 2020, estimates put 90% of mobile devices as NFC-enabled. The list of NFC-enabled mobile devices on Wikipedia is ~ 500 devices long.

With the average smartphone replacement cycle of 2.5 years, it’s probably safe to assume that 95% of US consumers are walking around with an NFC-enabled device in their pockets. This means that there’s no reason a merchant couldn’t get a legitimate NFC device to take payments for $50-$100.

Another impediment that looks non-trivial is contactless card penetration rates. One way consumers can use SoftPOS is through a contactless card. In the US, Visa announced in 2021 that 300M US Visa cards were NFC-enabled (i.e. contactless or tap to pay cards). At the end of 2022 the US had over 2B cards in circulation, meaning that a small percentage of US cards are actually capable of using NFC technology.

A 2020 report from the Philadelphia Federal Reserve supported these figures to show the low percentage of NFC-enabled cards in the US.

This lags far behind contactless payments in Canada, where 98% of cards are already NFC-enabled and represent 30% of payment volume.

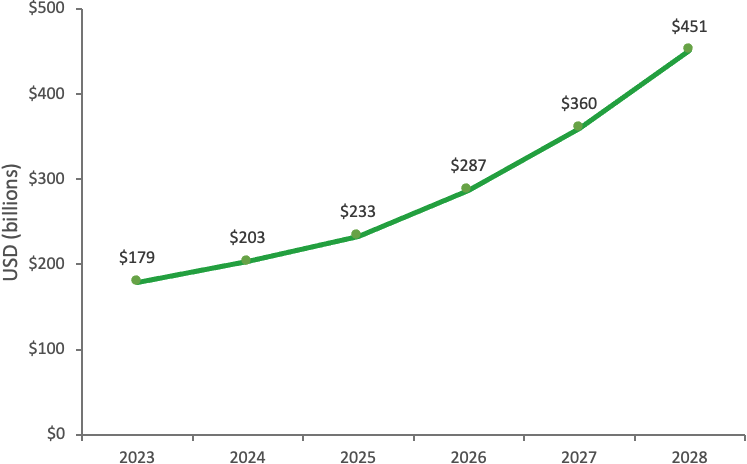

The other NFC-enabled payment modality is via mobile consumer devices. Again, this looks like a real impediment for SoftPOS. Research forecasts that US digital wallet NFC volume will grow to $451B by 2028, but that’s out of a universe of what is bound to be $12T of US card spend, or a meager 3.75% of volume. The irony, of course, is that payments made via a consumer wallet that combined biometrics with mobility should bring down the cost of payments as risks of fraud drop precipitously.

The reality is that mobile wallets aren’t really solving a problem in more mature payments markets. While research projects that half of global in-person payments volume will be contactless by 2027, an anemic $200B will be from digital wallets.

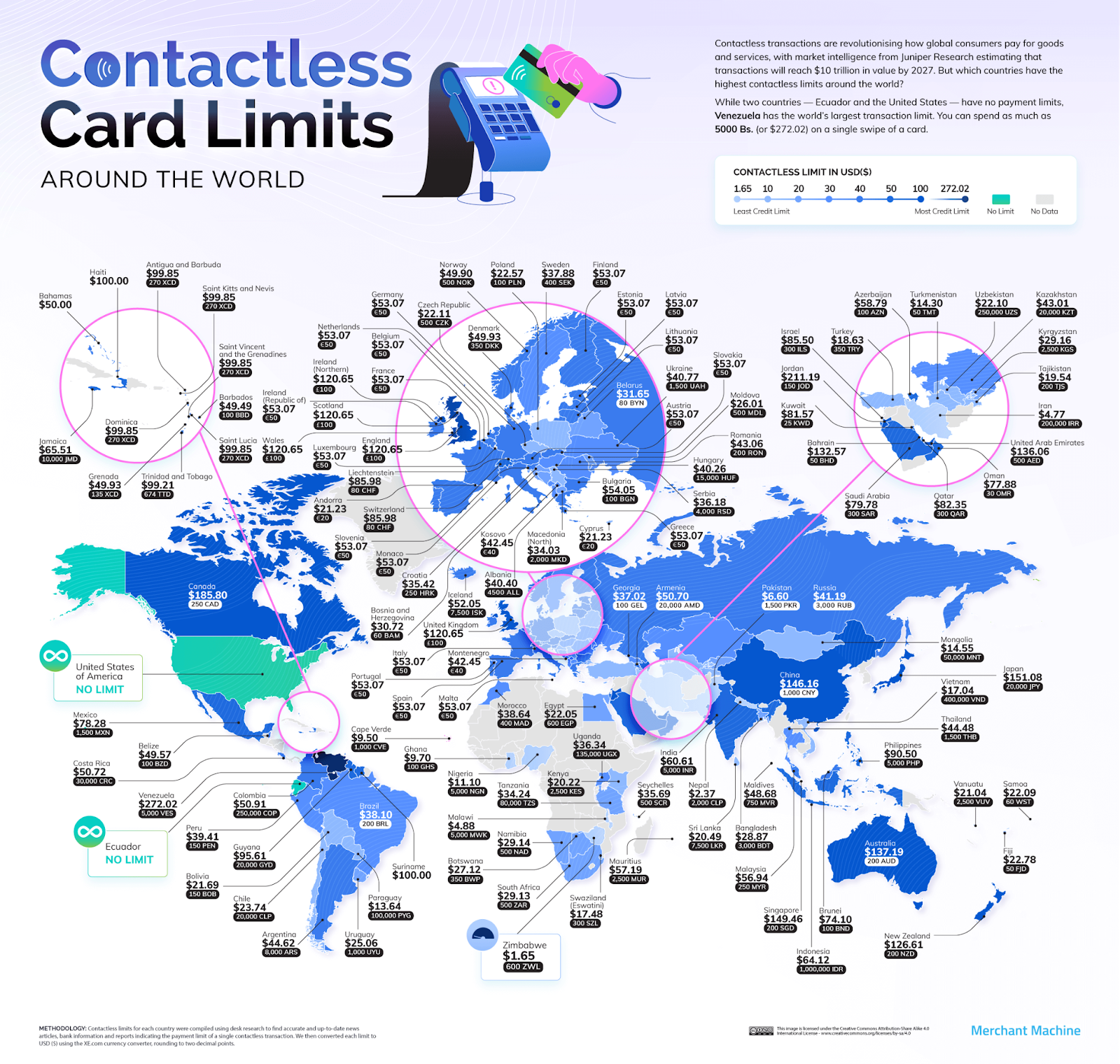

It doesn’t help that contactless limits are pretty low, with a contactless card maxing out at around $200 depending on the country and issuing bank, who ultimately sets the limits. In the US there is no contactless limit, which should be a boon to contactless if and when SoftPOS becomes more widely available.

So while payments would be cheaper with SoftPOS (lower hardware prices for NFC-enabled merchant devices and lower transaction costs with decreased risks from NFC-enabled mobile wallets), you still need consumers to actually use NFC for merchants to realize the economic benefits (and by the way, the savings from decreased fraud would never get passed to the merchant).

The best way to expedite the adoption of SoftPOS?

Very aggressive surcharge/cash discount programs that merchants foist upon consumers.

Imagine a 10% discount for paying with a bank app via NFC.

Think that wouldn’t drive consumers to use their bank to pay?

Surcharging of this magnitude would lead to a massive increase in SoftPOS adoption since people would be very motivated to avoid a 10% tax. This in turn would drive merchants to use SoftPOS devices in their stores.

SoftPOS by itself will not win the war. It’s a great tool, but it needs the support of rational policies (i.e. unlimited surcharging) to take its rightful place on the podium of payments innovation.

Remember: If you’re not bringing the cost of payments down, you’re fighting on the wrong side.

Believe there is a typo above, $1200 of $500k is 0.24% not 2.4%, did you mean to say $50k in revenue?

good catch! Updating