We’ve earmarked this article to be forever free in the event that any of the four literate restaurateurs somehow stumble onto this and, by an unforeseen miracle, learn something.

For all other restaurant operators just ignore this and go back to your sock puppets and paper mache: Mommy and Daddy are talking.

But you didn’t understand that because, well, you can’t read.

Let’s show how clandestinely greedy Toast’s new surcharging program is using some basic arithmetic.

We’ll start by assuming that interchange – the non-negotiable cost of payments that’s split between the duopoly card schemes (V/MA) and the issuing banks – is 2%.

Using the current – yet totally arbitrary – surcharging cap of 3%, a processor like Toast stands to make 1% of a merchant’s GPV (gross processing volume) in effective payments profit.

That’s because if the merchant charges the customer 3%, 2% covers the entirety of the interchange costs and what remains (1%) goes right into the processor’s coffers.

Huzzah!

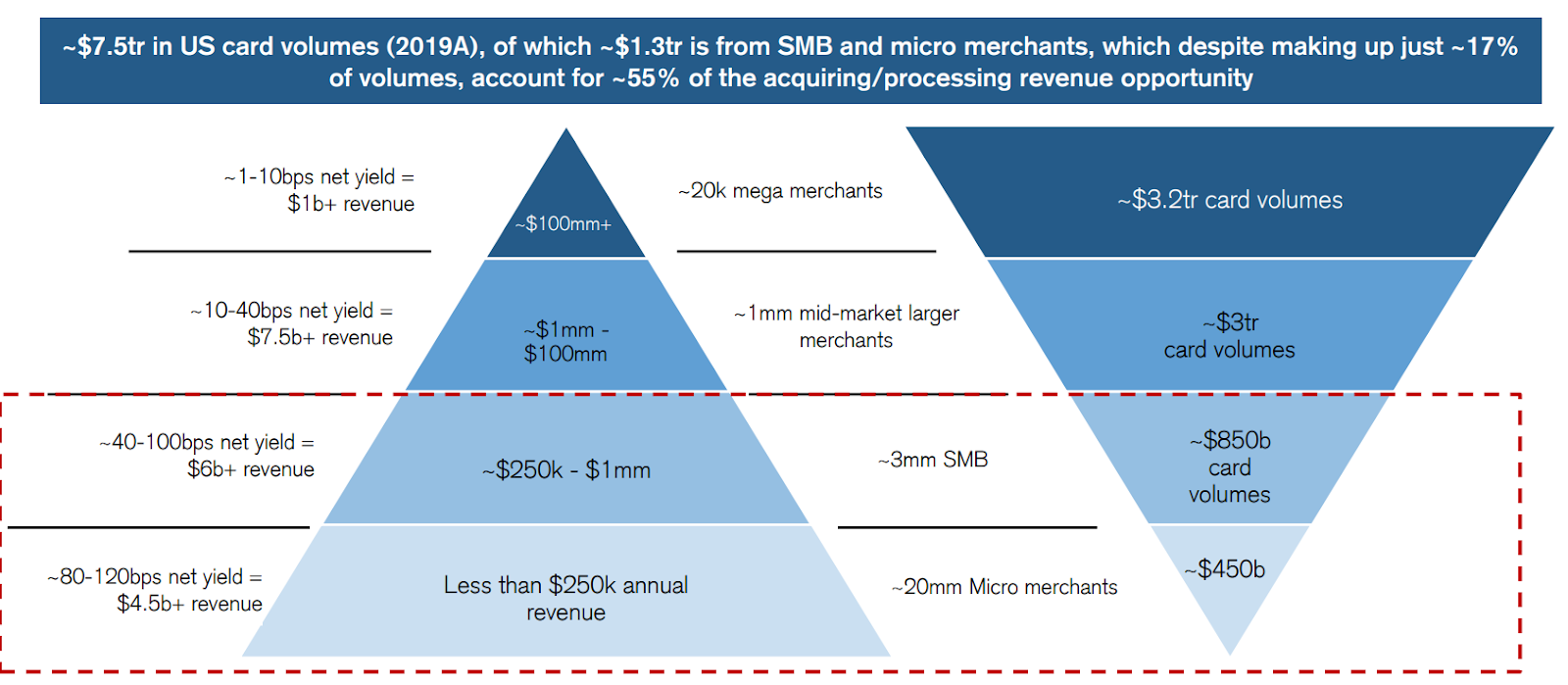

As a reminder of “fair” processing rates, let’s examine the average Toast merchant processing volume:

Toast counts 120,000 merchants doing $160B a year in GPV.

That’s $1.33M per location.

Using this graphic from Credit Suisse (at least we think that’s who published it) we can see the merchant GPV inside the pyramid on the left, and the expected take rates to the left of that. For example, for a merchant doing less than $250K of GPV (bottom of the left handed pyramid), the take rate (i.e. margin above interchange) is 80-120 bps (0.8% – 1.2% of merchant GPV).

The range ultimately depends on the greed of the processor, and the merchant’s MCC (merchant category code), meaning some MCCs (like restaurants, where Toast operates) are on the lower end of the range because the MCC in itself isn’t profitable enough to support higher payment margins.

Anecdotally (but based upon a healthy mountain of data), we can tell you that a restaurant doing $1.33M in card volume should be paying ~ 15 bps of payments margin.

Toast’s disclosed payments margins/take rates are ~45 bps.

We’re actually skeptical that Toast’s take rate has held steady at ~ 45 bps while needing to show further growth as a public company. To underscore our skepticism, we’ve seen Toast categorizing payments revenue as software revenue, likely to get the software multiple arbitrage in the market.

For example, Toast merchants remit to Toast a 50 bps fee for activating online ordering; that fee shows up on the merchant’s invoice as a “Technology Service Fee”, not as a payments fee, though it is clearly, 100% tied with payments volume and not a flat SaaS fee.

We actually think Toast merchants are paying somewhere closer to 80-90 bps of margin.

If you’re following us so far, here’s a graphic to demonstrate Toast’s payments margin prior to surcharging:

Keep in mind that even though Toast is earning 3x the “fair” payments rate on their merchants, their merchants are still paying the full list price for Toast’s software. Toast is only discounting hardware and installation services, and you can clearly see why: their customers are overspending on nearly-pure-EBITDA-payments by 3x.

With a 3% surcharge, Toast’s payments take rate nearly doubles to 100 bps, or 1%. This means Toast is earning more than 6x the “fair” payments rate.

In today’s market, payment processors have been pretty consistent on their positioning:

if the merchant surcharges 3%, the merchant pays nothing for processing.

That’s because, pursuant to the graphic from Credit Suisse, the processor stands to make substantially more money in a surcharge program than if they boarded the merchant traditionally. This breaks down at the micro merchant level, where a surcharge is close to parity with conventional processing, but those aren’t Toast’s customers so we’re not going to worry about it.

Without a hint of doubt, any Toast merchant could go to any processor and have all their processing fees waived if the merchant agreed to surcharge 3%.

Because, as our surcharging graphic makes clear, the processor stands to make 6.67x as much money in the surcharge program.

But apparently that’s not enough for Toast.

Toast’s positioning is genius.

Toast tells their merchants that if they surcharge 3%, their current processing bills will be lowered.

That’s right, the merchant will still have to pay for processing.

By how much will Toast lower the bill? It’s unclear, but we’ve seen Toast cut the merchant’s rates in about half.

If we use the very conservative math that Toast merchants are only paying 45 bps above interchange, which we’re still assuming is 2%, then a Toast merchant is currently paying 2.45% to accept payments with Toast.

Cutting this in half, the merchant will remit to Toast ~1.25%.

But remember this is only if the merchant agrees to surcharge 3%, where we made clear in an earlier graphic that Toast would clear 1% from the surcharge margin.

Because the 2% interchange cost is already covered in the 3% surcharge, Toast is making 1.25% + 1% = 2.25%.

Toast has (potentially) single-handedly increased the cost of dining at 120,000 restaurants by 4.5%.

God bless payments.

Truly the pinnacle of American innovation.

This is really interesting Jordan. I think it would be super interesting if you did a direct comp between ShiftFour and Toast…total cost of ownership analysis would be really interesting, as well as just a breakdown on surcharge and payment processing costs.

There’s too much variability to give you anything directional